Managing money well often comes down to having a clear plan—and sticking to it. The 50/30/20 budget rule is one of the simplest and most practical ways to organize your income. Instead of tracking every dollar, it breaks your spending into three broad categories, helping you balance needs, wants, and financial goals.

In this guide, we’ll break down exactly how the 50/30/20 rule works, why it’s useful, and walk through examples so you can see how to apply it in your own life.

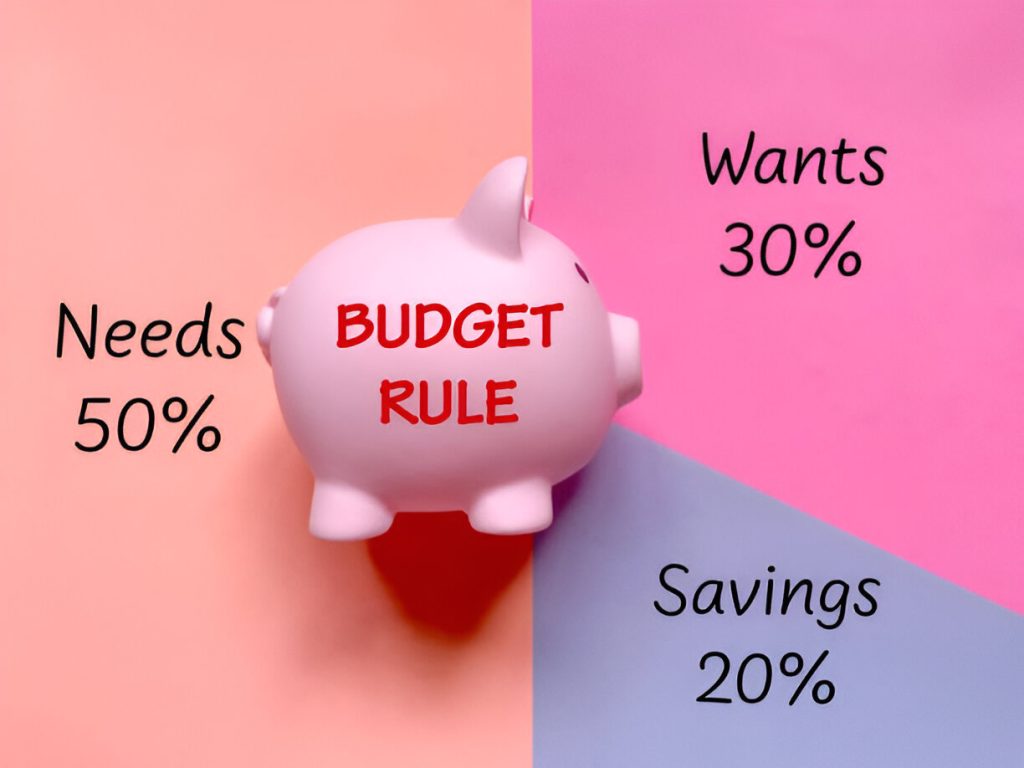

What Is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a popular guideline for dividing after-tax income into three basic categories:

- 50% for needs

- 30% for wants

- 20% for financial goals like savings and debt repayment

This approach was popularized by Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan. Its appeal comes from its simplicity. Rather than tracking every purchase, it encourages broad spending categories that are easy to follow and adapt.

Breaking Down Each Category

Let’s take a closer look at what each section includes and how it works.

50% for Needs

Needs are expenses you must pay to maintain a basic standard of living. These are essential costs that you can’t easily cut or go without.

Common examples include:

- Rent or mortgage payments

- Utilities (electricity, water, gas)

- Groceries

- Transportation (gas, public transit, car insurance)

- Minimum debt payments

- Health insurance and medical costs

If your needs exceed 50% of your income, you may need to adjust—by finding ways to lower fixed costs or rethinking housing, insurance, or transportation choices.

30% for Wants

Wants are the non-essentials—the things that add enjoyment or comfort to your life but aren’t necessary for survival. This is often the area with the most flexibility and the greatest opportunity to control spending.

Examples of wants include:

- Dining out

- Streaming subscriptions

- Shopping for clothes, electronics, or hobbies

- Gym memberships

- Vacations and entertainment

- Upgrades like premium cable or high-end gadgets

Being honest about what qualifies as a “want” can help you make better decisions when budgeting. If an expense isn’t absolutely necessary to live or work, it likely belongs in this category.

20% for Financial Goals

This final category is all about building your future. It includes debt repayment beyond minimums, retirement contributions, investments, and savings. The goal here is to use this portion of your income to improve your financial health and prepare for emergencies or long-term goals.

Here’s what typically falls under this 20%:

- Emergency fund contributions

- Retirement accounts (IRA, 401(k), etc.)

- Investments (brokerage accounts, CDs)

- Extra debt payments (credit cards, student loans)

- Savings for goals like a home, car, or education

If you’re carrying high-interest debt, consider using this section to aggressively pay it down before prioritizing long-term savings. Once that debt is reduced, more of your income can shift toward building wealth.

Example of the 50/30/20 Budget in Action

Let’s walk through a realistic example so you can see how this budget rule works with real numbers.

Monthly Take-Home Income: $4,000

Based on the 50/30/20 rule:

- 50% for Needs = $2,000

- 30% for Wants = $1,200

- 20% for Financial Goals = $800

Here’s how that might look when broken down:

Needs ($2,000)

- Rent: $1,200

- Utilities: $150

- Groceries: $400

- Transportation: $250

Wants ($1,200)

- Restaurants and takeout: $300

- Streaming services: $50

- Shopping and hobbies: $300

- Travel fund: $200

- Entertainment: $350

Financial Goals ($800)

- Retirement account: $300

- Emergency fund: $250

- Credit card payment (extra): $250

This framework gives structure to your spending and makes it easier to prioritize the most important financial areas.

Why the 50/30/20 Budget Rule Works

There are many reasons why this budgeting method has gained popularity. It’s simple, flexible, and avoids the overwhelm that can come with tracking every transaction. Here are a few of the biggest advantages:

It Promotes Balance

Many people either overspend or save without a plan. This rule provides a structured way to cover necessities, enjoy life, and make financial progress at the same time.

It’s Easy to Follow

You don’t need apps, spreadsheets, or detailed ledgers. With just three main categories, it’s accessible even for those who are new to budgeting.

It Adjusts With Your Income

Whether you earn $3,000 a month or $10,000, the 50/30/20 rule scales. The percentages stay the same, allowing you to maintain consistency even as your income changes.

It Encourages Long-Term Thinking

By allocating 20% toward financial goals, this rule keeps future planning front and center. It’s a reminder to pay yourself first, even while managing everyday expenses.

When the 50/30/20 Rule Might Not Fit

Although the rule is useful, it’s not perfect for everyone. Personal circumstances, debt loads, or regional cost-of-living differences can make the 50/30/20 split difficult to apply exactly.

For example:

- If you live in a high-cost city, your rent alone may exceed 50% of your income.

- If you’re aggressively paying off debt, you may want to allocate more than 20% to financial goals.

- If you’re saving for a large purchase, like a house down payment, you may temporarily reduce wants to boost savings.

The key is flexibility. Use the 50/30/20 rule as a starting point, not a hard rule. You can shift the percentages slightly to match your situation while still following the spirit of the framework.

Tips for Making the Rule Work for You

Here are a few ways to customize the 50/30/20 budget and make it work in real life:

Use Automatic Transfers

Set up automatic transfers to your savings or investment accounts to remove the temptation to spend that money elsewhere.

Track Spending for a Month

Before diving in, track your spending for 30 days. This helps you understand your current habits and identify areas where you’re over or under the suggested percentages.

Adjust Over Time

Your budget is a living document. Life events, raises, or new expenses may require you to revisit your budget and make updates.

Keep Wants in Check

Be mindful of “lifestyle creep”—spending more on non-essentials as your income grows. Sticking to the 30% guideline helps keep spending aligned with your values and goals.

Final Thoughts

The 50/30/20 budget rule is a straightforward way to take control of your money. By dividing your income into clear categories—needs, wants, and financial goals—it creates a sustainable plan that balances today’s needs with tomorrow’s priorities.

While it may not work for every situation exactly as written, it provides a strong framework to build from. And when you consistently set aside time for budgeting and allocate part of your income to savings, you’re making progress toward long-term financial stability—one decision at a time.